- Integrated Planning

Integrated Planning

Integrated planning is a sustainable approach to planning that builds relationships, aligns the organization, and emphasizes preparedness for change.

- Topics

Topics

- Resources

Resources

Featured Formats

Popular Topics

- Events & Programs

Events & Programs

Upcoming Events

- Community

Community

The SCUP community opens a whole world of integrated planning resources, connections, and expertise.

- Integrated Planning

Integrated Planning

Integrated planning is a sustainable approach to planning that builds relationships, aligns the organization, and emphasizes preparedness for change.

- Topics

Topics

- Resources

Resources

Featured Formats

Popular Topics

- Events & Programs

Events & Programs

Upcoming Events

- Community

Community

The SCUP community opens a whole world of integrated planning resources, connections, and expertise.

Planning for Higher Education Journal

Planning for Higher Education JournalA Guide for Optimizing Resource Allocation

Link Assessment, Strategic Planning, and Budgeting to Achieve Institutional Effectiveness From Volume 48 Number 2 | January–March 2020By Dania Salem, Hiba Itani, Ali El-HajjPlanning Types: Resource PlanningChallenges: Planning Alignment

From Volume 48 Number 2 | January–March 2020By Dania Salem, Hiba Itani, Ali El-HajjPlanning Types: Resource PlanningChallenges: Planning AlignmentThe article presents a framework for integrating assessment, strategic planning, and resource allocation at all levels of an institution. For that purpose, data are collected from academic departments and non-academic units. They are then integrated with strategic planning metrics into an assessment report that identifies the resources that need to be allocated, and to evaluate progress toward developing a strategic plan. The framework can be applied at the departmental or unit level, as well as at the institutional level. It provides valuable input for the budget process and can be used for updates in strategic planning.

DOWNLOAD3 Takeaways . . .

. . . For Using Research to Guide Asset Apportionment- Explore best practices for assessment, strategic planning, and budgeting processes.

- By programs/units, colleges, and at the institution level, evaluate the link between assessment, strategic planning, and budgeting processes.

- Integrate assessment findings to inform institutional planning and decision-making related to budgeting and resources allocation.

Introduction

Most colleges and universities have well-established processes for assessment, strategic planning, and resource allocation. Those processes are often disconnected in practice (Middaugh 2009), which results in inefficient allocation of resources. Reinforcing the link between assessment, strategic planning, and budgeting is important for meeting accreditation standards, for better use of assessment results, and for ideal allocation of resources. Accreditation standards require institutions to demonstrate institutional effectiveness by providing documented evidence that all activities using institutional resources support the institution’s mission (Hinton 2011; Hollowell, Middaugh, and Sibolski 2006).

Reinforcing the link between assessment, strategic planning, and budgeting is important for meeting accreditation standards, for better use of assessment results, and for ideal allocation of resources.

In light of the requirements issued by regional accrediting agencies to demonstrate institutional effectiveness, higher education institutions are greatly concerned with bridging the gap between assessment and decision-making—and effectively linking assessment, planning, and budgeting processes (Middaugh 2009). In this article, we present a framework for connecting assessment, strategic planning, and budgeting processes at higher education institutions to optimize resource allocation.

Assessment

According to Banta and Palomba (2014), the term assessment is commonly used to measure student learning, but it can also be used to evaluate academic programs, academic support services, and administrative services. Assessment happens at the academic, non-academic, and institutional levels of the college or university. Different assessment practices and processes often exist at each level.

Academic Assessment

Academic assessment practices include appraisal of program learning outcomes, periodic program reviews, and program accreditations, which happen at the level of program, academic department, and college/school. Academic assessment practices often result in a set of recommendations or actions for improvement.

Assessment of program learning outcomes is widely used in higher education institutions as a means of evaluating student learning achievement in academic programs (Banta and Palomba 2014). Periodic program reviews are usually conducted at the academic department level and address areas such as teaching, research, student enrollment, and instructional facilities, in an effort to assess the quality of academic programs and identify areas for improvement (Hollowell et al. 2006). Program reviews often consist of preparing a self-study by the department, which is then followed by an external evaluation that results in an improvement plan. Academic programs, departments, or colleges may also seek accreditation by a specialized professional accrediting body that evaluates the extent to which a department or program maintains a set of standards and practices that are deemed to be of high quality (Wuest 2017).

Non-Academic Assessment

Assessment also happens at the level of non-academic units, which include administrative and academic support divisions. Although assessment processes in non-academic units are less common than assessment processes for academic units, they can occur through periodic reviews (White 2007) and outcomes assessment (Banta and Palomba 2014) for the purpose of improving service offerings (Nichols & Nichols 2000). Those processes can also result in a set of recommendations or actions for improvement.

Periodic unit reviews resemble occasional program reviews: Units prepare a self-study report and invite external reviewers to evaluate the unit and the quality of its services (Middaugh 2011). The unit review usually results in a set of recommendations for improvement that is based on the requests of the unit and the observations of the external reviewers. Unit outcomes assessment resembles program learning outcomes assessment. However, it focuses on the functions, processes, and services offered by the unit, rather than learning outcomes acquired by students upon completion of an academic program (Nichols & Nichols 2000). By measuring a set of key performance indicators and comparing them to preset targets, unit outcomes assessment determines whether the unit’s functions and services are being performed properly (UCF Administrative Assessment Handbook 2008).

Institutional Assessment

One of the major types of institutional assessment is regional institutional accreditation, which provides the university and the accrediting agency with insight into areas where the institution meets or exceeds expectations and where areas for improvement exist. Another type of institutional assessment is a performance evaluation of the university’s strategic plan through tracking selected metrics and comparing them to targets. That method is commonly used to evaluate the implementation of the institutional strategic plan and monitor the achievement of the institutional goals.

According to Wuest (2017), different appraisal practices should be well integrated, and the link should be made evident to stakeholders to reinforce a culture of continuous improvement where faculty, staff, and administrators are motivated to participate in assessment activities (Aloi 2005). Having that integrated view of assessment at the institutional level serves several purposes: identifying interactions among different programs, helping students achieve institution-wide learning goals, supporting resource allocation decisions, and demonstrating institutional effectiveness to external stakeholders (Miller and Leskes 2005).

Strategic Planning

Strategic planning is a systematic and data-based process, which helps organizations set their priorities, build commitment, and allocate resources (Allison & Kaye 2011). According to Hinton (2011), the foundation of the strategic plan is the institutional mission statement, which is a basic declaration of purpose that delineates why an entity exists and what it intends to achieve. Strategic goals and objectives are considered the basic elements of the strategic plan. The implementation plan helps turn the goals and objectives into a working proposal. It documents the responsible entity for implementing an action, a deadline for every action, and a measure to assess the progress toward the completion of the action (Hinton 2011).

Successful strategic planning is characterized as being integrated, strategic, and aligned (Norris & Poulton 2008).

Integrated, Strategic, and Aligned Planning

Successful strategic planning is characterized as being integrated, tactical, and aligned (Norris & Poulton 2008). Integrated planning takes a comprehensive view: Academic, resource, and facility planning are all interconnected. For planning to be strategic, it should define what the institution as a whole unit should do, taking into consideration external factors. In addition, alignment of activities such as strategic planning, capital planning, accreditation, and performance management across the college, department, and unit levels is important for successful planning (Norris & Poulton 2008).

Strategic Planning Across the Institution

Strategic planning happens at different levels of the institution. At the level of academic departments, colleges, and schools, each academic dean is responsible for developing strategic plans for the school, while each department chairperson formulates a strategic plan for the department (Nauffal and Nasser 2012). Strategic planning at the level of non-academic units focuses on the means through which to contribute toward meeting institutional goals and serving the institution (Nichols & Nichols 2000).

Academic and non-academic strategic plans are typically interconnected with the institutional strategic plan. Some institutions follow a top-down approach where administrators lead institutional planning activities, some institutions utilize bottom-up movements, and others use a mixed approach (Brinkhurst, Rose, Maurice & Ackerman 2011). Bottom-up strategic planning is characterized as participative, and division managers play an important role in the process. Higher-level administrators do most of the planning at institutions that follow a top-down strategic planning approach (Dutton & Duncan 1987).

Cowburn (2005) argued that top-down and bottom-up approaches have both proven to result in failure. A balanced method where top-down meets bottom-up is required for institutions to effectively formulate and implement their strategic plans. Simply collecting objectives from different levels of the institution does not make a strategic plan, and dictating strategic goals without consultation doesn’t lead to coherent and effective planning. Consulting with academic departments and administrative units is essential when setting strategic priorities for the institution. Once those priorities are set, individual units need to link their plans to the university’s objectives in a consistent and structural way (Cowburn 2005).

Strategic Plan Assessment

In order to monitor the implementation of the strategic plan, an assessment that includes the frequency of evaluation, the objectives to be measured, entities that will conduct the appraisal, the methods, and how the results will be utilized for decision-making is used (Trettel & Yeager 2011). In general, key performance indicators are identified for each objective of the strategic plan in order to provide quantitative and qualitative insight about the achievement of the intended outcomes (Trettel & Yeager 2011).

Budgeting

The most common budgeting models for institutional resource allocation are incremental budgeting, formula-based budgeting, zero-based budgeting, performance-based budgeting, responsibility-center budgeting, and initiative-based budgeting (Goldstein 2012). There is no one perfect budgeting model for all institutions, and some colleges and universities may choose to implement a hybrid model by combining components from two or more budgeting models. A summary of the common budgeting models with their description and pros and cons is included in figure 1.

Program prioritization decisions include addition, reduction, consolidation, restructuring, or elimination of programs based on assessment results (Dickeson 2010).

Figure 1 Common Budgeting Model

Budgeting Model

Description

Pros

Cons

Incremental budgeting model Budget adjustments are based on a previously allocated base budget from the previous year with percent increase or decrease. - Simple

- Most widely used in higher education

- Does not rely on assessment data or improvement plans

- A department with insufficient resources may not be granted its needed resources

Formula-based budgeting model It is mainly used in public institutions. It relies heavily on quantitative measures to distribute resources and predict future resource needs, depending on program cost and demand. - Aligned with assessment

- Programs are funded even if they are not aligned with the university mission

- Programs with decreasing enrollment may not be funded

Zero-based budgeting model It usually starts with a zero-base amount or a low percentage of last year’s budget as a base. It estimates the resource needs of each activity independently. - Aligned with assessment

- Time-consuming

- Difficult to implement at the institutional-level

Performance-based budgeting model It allocates resources based on the achievement of specific targets in a program. - Aligned with assessment

- Difficult to implement accurately because of its quantitative nature

Initiative-based budgeting model Only activities or programs that align with key initiatives are funded. - Aligned with strategic planning

- Creates a very competitive resource allocation environment

Responsibility-center budgeting model A school is credited with the tuition revenues generated by classes taught by its faculty. The tuition revenues are usually under the dean’s control.

- Each school manages and controls its own revenues and expenses

- Creates competition among faculties to recruit and attract the greatest number of students each year

Data from Goldstein (2012)

Integrating Assessment, Strategic Planning, and Budgeting Processes

Linking Assessment and Strategic Planning

The link between strategic planning and assessment is two-way, where assessment results inform strategic planning efforts and provide evidence of meeting institutional outcomes. On the other hand, the strategic plan supports the assessment process by providing a framework for revising assessment outcomes and driving program reviews and accreditation efforts (Wuest 2017). According to Aloi (2005), to establish an effective link between strategic planning and assessment, both should be part of an ongoing and decentralized process where all levels of the university undergo evaluation and use the results for planning purposes.

Linking Assessment and Budgeting

Higher education institutions should streamline their assessment processes—for example, improvement plans resulting from activities such as periodic reviews—in a way to collect data that can inform the budgeting process (Trettel & Yeager 2011). Dickeson (2010) noted that the majority of resources in higher education institutions are consumed by programs. According to him, proper reallocation of resources can be achieved through a rigorous and effective program prioritization process. The programs are ordered based on a list of 10 criteria, which may be modified by the institution. Data related to each criterion are collected and can be benchmarked with other institutions. Stronger programs are rewarded by allocating additional resources to them, while weaker programs receive a reduced budget. Program prioritization decisions include addition, reduction, consolidation, restructuring, or elimination of programs based on assessment results (Dickeson 2010).

Linking Strategic Planning and Budgeting

Because higher education institutions have a limited budget to allocate per year, it is important to prioritize and assign funds to the most rewarding and strategic activities, projects, or initiatives. In general, there should be a strong link between strategic planning and budgeting: Activities that are directly linked to strategic key priorities are funded, while other activities based merely on people’s wishes are not funded. According to Stack and Leitch (2011), integrated planning occurs when planning and budgeting processes are coordinated in an effective manner at different levels of the institution and in alignment with the institutional mission and priorities. Even though the main components of an integrated planning framework are common in most institutions, Stack and Leitch (2011) recommended that each institution develop its unique framework, taking into consideration its culture.

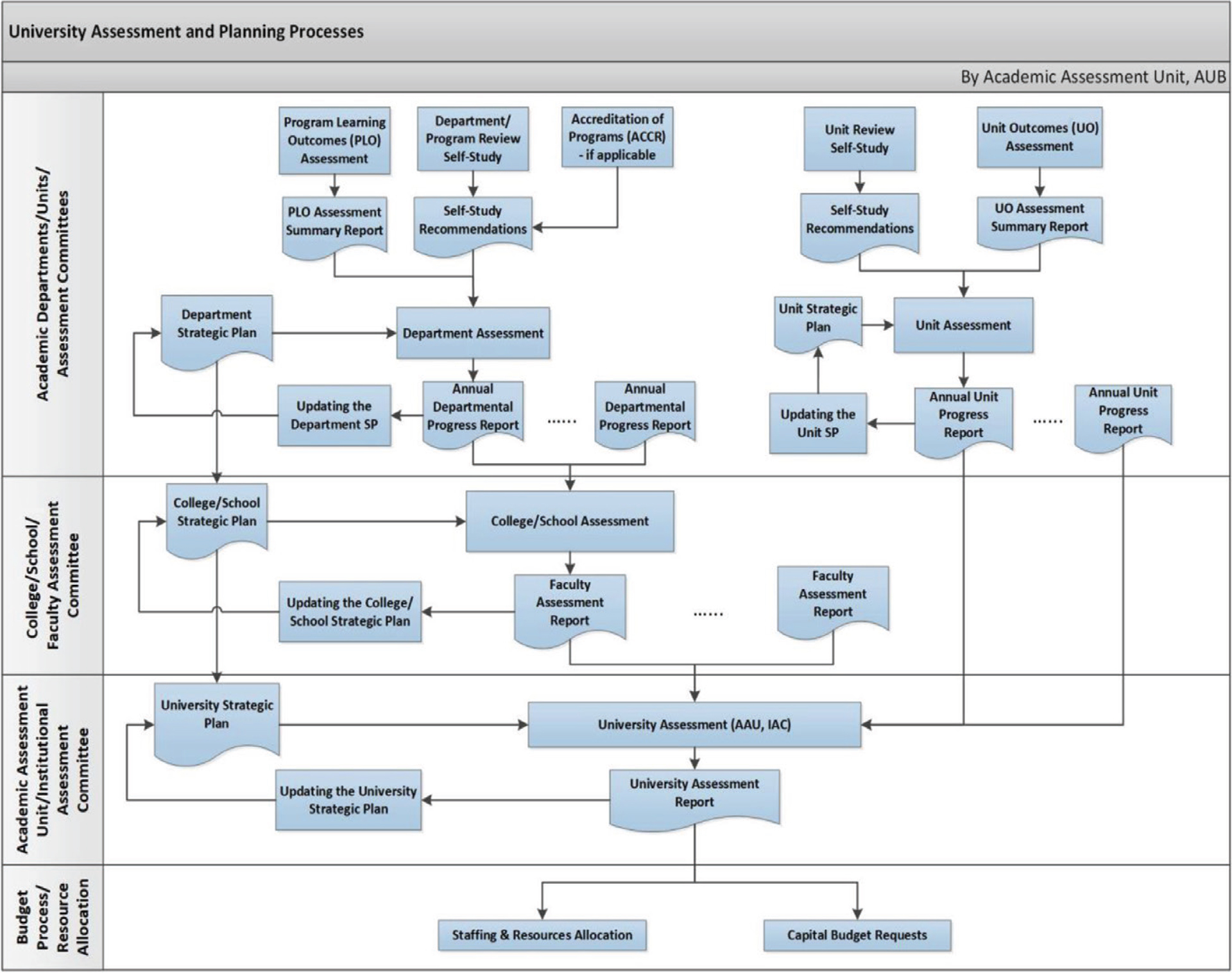

Framework for Linking Assessment, Strategic Planning, and Resource Processes

In order to integrate assessment, strategic planning, and resource allocation processes, we created a linking framework as shown in figure 2. The framework reflects the two-way link that exists between assessment processes and strategic plans—and comprises decentralized and ongoing processes, which happen at all levels across the university. As shown in figure 2, different processes exist at different levels of the institution, and findings are used to update the corresponding strategic plan at each level.

Figure 2 Framework for Integrating Assessment, Strategic Planning, and Resource Allocation

Click image to view larger.

To integrate resource allocation processes with assessment and strategic-planning processes, it is important to align all cycles.

We developed the framework at American University of Beirut (AUB) in response to the accreditation standards related to closing the loop between assessment, planning, and resource allocation. At AUB, the main entities involved in that process were the Academic Assessment Unit, the Institutional Assessment Committee (IAC), the Office for Financial Planning, and the Planning and Budgeting Committee; therefore, we based our framework assuming the existence of those entities. Although most colleges and universities do not have those exact same units, they may have different ones with similar responsibilities. Depending on their organizational structure, assessment processes, strategic planning processes, and resource-allocation methods, higher education institutions can adapt the framework by using the same main components and customizing the details.

Our framework begins with the more detailed assessment and strategic plans occurring at the level of academic departments and non-academic units. It then moves up to the level of college and faculties, and, finally, to the level of the institution as a whole. The assessment and strategic planning conducted at the level of faculties incorporates the feedback from departments; the assessment and strategic planning at the level of the institution includes feedback from colleges and non-academic units. At all levels, assessment results are organized into annual progress reports that include planned actions for improvements with their estimated resources attached. Strategic plans are developed at all levels through a balanced top-down and bottom-up approach. All strategic plans are updated based on assessment findings.

At the level of academic departments, an assessment committee is formed and prepares an annual progress report. That includes improvement plans and recommendations resulting from all assessment processes—with relevant intended actions and estimated resources noted. By the end of the academic year, all academic departments submit to the dean’s office their college’s/school’s annual departmental progress reports. They detail their progress in implementing the improvement actions that resulted from the periodic program review, program learning outcomes assessment, strategic-planning initiatives, and/or accreditation processes. At the level of colleges and schools, all departmental progress reports collected from all respective academic departments are compiled to develop annual faculty assessment reports. Those annual reports are augmented with the results of the evaluation of college/school strategic plans, which include activities, requested resources, and an estimated timeline for implementation.

Non-academic units perform ongoing assessment activities similar to those conducted by academic departments. Unit outcomes assessment, periodic unit reviews, and the performance evaluation of unit strategic plans, if available, are compiled. Those annual unit progress reports list activities completed during the previous year, along with planned activities and their estimated resources.

At the institutional level, the academic assessment unit collects the annual faculty assessment reports and the annual unit progress reports from all colleges and units. AAU compiles those reports and the assessment results of the institutional strategic plan to generate the University Assessment Report (UAR). The UAR includes the university’s overall assessment plan and a list of improvement actions and requested resources. All planned activities are categorized and linked to the institutional strategic goals, objectives, or initiatives in the UAR. By assigning categories to activities, similar actions across the university can be easily grouped and their resource requests isolated. Additionally, linking activities to the institutional strategic plan lets administrators identify the highest-priority actions, those that are needed to achieve the institutional goals, objectives, or initiatives.

The Institutional Assessment Committee (IAC), which is formed of representatives from all faculties and non-academic units, provides leadership in the implementation of the different university assessment processes, ensuring the integration of findings with strategic plans and resource allocation. The IAC reviews the UAR, provides feedback, and approves improvement plans submitted by all departments and units. The IAC also identifies the highest-priority activities that have direct links to key initiatives of the institutional strategic plan.

The Office for Financial Planning links capital budget requests to the recommendations received from IAC. Non-recurring operating budget requests are also linked to those recommendations. The Planning and Budgeting Committee reviews all operating and capital budget requests collected from different internal constituencies. The budget requests related to high-priority activities, projects, and initiatives resulting from assessment are allocated immediately—because they are aligned with the institution’s key priorities. Other budget requests that are not linked to the improvement plan or to the institutional strategic plan are postponed or not granted. Based on assessment data, strategic plans, capital and operational requests, and available budget, all stakeholders decide on resource allocation for the following year. Consequently, the framework ensures the distribution of resources based on strategic priorities, assessment results, and stakeholder feedback.

To integrate resource allocation processes with assessment and strategic-planning processes, it is important to align all cycles. Because the assessment and strategic planning cycles are based on the academic year—while the budgeting cycle is based on the fiscal year—a two-year timeline can be adopted, where assessment data collected in one year are used to inform the next year’s budget. Therefore, the progress report filled by departments and units should include the list of improvements resulting from assessment findings, the planned actions for coming years, and the estimated resources for implementing those actions.

Based on assessment data, strategic plans, capital and operational requests, and available budget, all stakeholders decide on resource allocation for the following year.

Conclusion

By linking assessment, strategic planning, and budgeting processes, results are better utilized, strategic plans reflect the real needs and priorities of the institution, and resources are distributed more effectively. In addition, the integration between assessment, planning, and budgeting can be used to improve internal processes, functions, and services, which is usually required for institutional accreditation. In order to ensure the successful implementation of the linking framework, it is extremely important to have strong support from the top administration, mainly the president, provost, and deans. Because ongoing assessment and regular reporting are essential for the success of the process, the buy-in of department chairs, faculty, and directors is needed. Colleges and universities can tailor the framework to reflect their own institutional structure and processes. While it is challenging to change processes in higher education institutions, having a documented link between assessment, strategic planning, and budgeting processes can help colleges and universities identify areas for improvement and address them to achieve institutional effectiveness.

References

Allison, M. & J. Kaye. Strategic Planning for Nonprofit Organizations: A Practical Guide and Workbook. San Francisco: Jossey-Bass, 2011.

Aloi, S. L. “Best Practices in Linking Assessment and Planning.” Assessment Update 17, no. 3 (2015): 4–6.

Banta, T. W. & C. A. Palomba. Assessment Essentials: Planning, Implementing, and Improving Assessment in Higher Education. New York: John Wiley & Sons, 2014.

Brinkhurst, M., P. Rose, G. Maurice & J. D. Ackerman. “Achieving Campus Sustainability: Top-down, Bottom-up, or Neither? International Journal of Sustainability in Higher Education 12, no. 4 (2011): 338–354.

Cowburn, S. “Strategic Planning in Higher Education: Fact or Fiction?” Perspectives 9, no. 4 (2005): 103–109.

Dickeson, R. C. Prioritizing Academic Programs and Services. San Francisco: Jossey-Bass, 2010.

Dutton, J. E. & R. B. Duncan. “The Influence of the Strategic Planning Process on Strategic Change.” Strategic Management Journal 8, no. 2 (1987): 103–116.

Goldstein, L. A Guide to College and University Budgeting: Foundations for Institutional Effectiveness, 4th ed. Washington, DC: National Association of College and University Business Officers, 2012.

Hinton, K. E. A Practical Guide to Strategic Planning in Higher Education. Ann Arbor: Society for College and University Planning, 2012.

Hollowell, D., M. F. Middaugh & E. Sibolski. Integrating Higher Education Planning and Assessment: A Practical Guide. Ann Arbor: Society for College and University Planning, 2006.

Middaugh, M. F. “Closing the Loop: Linking Planning and Assessment.” Planning for Higher Education 37, no. 3

(2009): 5.Middaugh, M. F. Planning and Assessment in Higher Education: Demonstrating Institutional Effectiveness. New York: John Wiley & Sons, 2011.

Miller, R. & A. Leskes. Levels of Assessment: From the Student to the Institution. Washington, DC: Association of American Colleges and Universities, 2005.

Nauffal, D. I. & R. N. Nasser. “Strategic Planning at Two Levels.” Planning for Higher Education 40, no. 4 (2012): 32.

Nichols, K. W. & J. O. Nichols. The Department Head’s Guide to Assessment Implementation in Administrative and Educational Support Units. New York: Agathon Press, 2000.

Norris, D. M. & N. L. Poulton. A Guide to Planning for Change. Ann Arbor: Society for College and University Planning, 2008, 99–120.

Stack, P. & A. Leitch. “Chapter 3: Integrated Budgeting and Planning,” in Integrated Resource and Budget Planning at Colleges and Universities. Edited by C. Rylee. Ann Arbor: Society for College and University Planning, 2011. 17–31.

Trettel, B. S. & J. L. Yeager. “Linking Strategic Planning, Priorities, Resource Allocation, and Assessment.” In Increasing Effectiveness of the Community College Financial Model. New York: Palgrave Macmillan, 2011.

“UCF Administrative Assessment Handbook,” 2008. Retrieved from University of Central Florida: http://oeas.ucf.edu/doc/adm_assess_handbook.pdf.

White, Eileen Knight. “Institutional Effectiveness: The Integration of Program Review, Strategic Planning, and Budgeting Processes in Two California Community Colleges” (PhD diss., St. Andrews University, 2007), https://digitalcommons.andrews.edu/dissertations/1539.

Wuest, B. “Connecting the Dots: Integrating Planning and Assessment.” Assessment Update 29, no. 2 (2017): 1–16.

Author Biographies

Ali El-Hajj, PhD, is a professor of electrical and computer engineering at American University of Beirut (AUB). His research interests include applied electromagnetism and machine learning. He has 35 years of academic experience, and he assumed leadership positions at AUB in general education, academic assessment, and strategic planning. El-Hajj received a master’s in engineering from L’Ecole Superieure d’Electricite, France, and a doctorate in engineering from University of Rennes I.

Ali El-Hajj, PhD, is a professor of electrical and computer engineering at American University of Beirut (AUB). His research interests include applied electromagnetism and machine learning. He has 35 years of academic experience, and he assumed leadership positions at AUB in general education, academic assessment, and strategic planning. El-Hajj received a master’s in engineering from L’Ecole Superieure d’Electricite, France, and a doctorate in engineering from University of Rennes I. Hiba Itani, M.Ed, is the policy and assessment officer at the Academic Assessment Unit at American University of Beirut (AUB). Her career interests include periodic assessment, strategic planning assessment, and policy development. She earned her M.Ed in higher education (institutional research) from PennState University, and a master’s in engineering management (financial and industrial engineering) and a BE in computer and communications engineering from AUB.

Hiba Itani, M.Ed, is the policy and assessment officer at the Academic Assessment Unit at American University of Beirut (AUB). Her career interests include periodic assessment, strategic planning assessment, and policy development. She earned her M.Ed in higher education (institutional research) from PennState University, and a master’s in engineering management (financial and industrial engineering) and a BE in computer and communications engineering from AUB. Dania Salem, M.Ed, is the assistant director at the Academic Assessment Unit at American University of Beirut (AUB). She coordinates assessment processes and prepares university assessment and strategic planning progress reports. She earned her M.Ed in higher education (institutional research) from PennState University, and a master’s in engineering management and a BE in computer and communications engineering from AUB. She has held several positions in software engineering, library management automation, and institutional research.

Dania Salem, M.Ed, is the assistant director at the Academic Assessment Unit at American University of Beirut (AUB). She coordinates assessment processes and prepares university assessment and strategic planning progress reports. She earned her M.Ed in higher education (institutional research) from PennState University, and a master’s in engineering management and a BE in computer and communications engineering from AUB. She has held several positions in software engineering, library management automation, and institutional research.Engage with the Authors

To comment on this article or share your own observations, message or email www.linkedin.com/in/dss00, www.linkedin.com/in/hiba-itani-08789277, or elhajj@aub.edu.lb.

- Topics

- Topics

- Integrated Planning

Integrated Planning

- Topics

Topics

- Resources

- Topics